| Table of Contents

| Function Reference

| Function Finder

| R Project |

RESAMPLING TECHNIQUES

Caveat emptor

Resampling techniques depend upon repeated (re)randomization or simulation

of a sample. Computers do not generate random numbers. Since an algorithm is

used to produce the results of a function like

runif(), these results are

technically referred to as pseudorandom. I've done a few casual tests of the R

random number generator, and it seems to be very good, but I'm not an expert on

pseudorandom number generators. So I will begin with a warning: Computer

intensive resampling is only as good as your pseudorandom number generator.

Further Notes

I am scratching the surface of resampling techniques in this tutorial. I

don't claim to have extensive knowledge, so the examples here will be fairly

simple, just to illustrate what resampling is and how it can be done in R.

Speaking of "how it can be done in R," those of you who may have read this

tutorial before it's latest revision have had an earful (eyeful?) of my

opinion of the boot() function and its help page.

FINALLY, someone has written a good, comprehensible explanation of the function

(Zieffler, Harring, and Long, 2011, see refs). I've

also found some good examples online. I will try to do

it a little more justice in this revision.

Concerning the "sleep" data set, which is used here: These data are

actually paired scores (see the help page), although they have often been

used as an example for unpaired tests. For the sake of illustrating how

things work, it doesn't really make much difference, but I just wanted to let

you know that I know these are paired scores. We'll use them both ways.

I will illustrate three basic techniques in this tutorial.

- Monte Carlo simulation

- Jackknife resampling (randomization test)

- Bootstrap resampling

Monte Carlo Estimation of Power

Although the term "resampling" is often used to refer to any repeated random

or pseudorandom sampling simulation, when the "resampling" is done from a known

theoretical distribution, the correct term is "Monte Carlo" simulation. I will

use such a scheme here to demonstrate how power can be estimated for the

two-sample t-test using Student's sleep data.

> data(sleep)

> str(sleep)

'data.frame': 20 obs. of 3 variables:

$ extra: num 0.7 -1.6 -0.2 -1.2 -0.1 3.4 3.7 0.8 0 2 ...

$ group: Factor w/ 2 levels "1","2": 1 1 1 1 1 1 1 1 1 1 ...

$ ID : Factor w/ 10 levels "1","2","3","4",..: 1 2 3 4 5 6 7 8 9 10 ...

> attach(sleep)

> tapply(extra, group, mean)

1 2

0.75 2.33

> tapply(extra, group, sd)

1 2

1.789010 2.002249

> tapply(extra, group, length)

1 2

10 10

The experiment is on the effect of a soporific drug. All subjects were

measured during a baseline (no-drug) period and again during the drug trial,

and the "extra" variable is how much additional sleep time they got over

baseline during the drug trial. Group 1 is the control (placebo) condition,

and Group 2 is the treatment (drug) condition. To make it easier to keep track

of this, I'm going to rename the levels of the "group" factor.

> detach(sleep) # NEVER modify an attached data frame!

> sleep$group = factor(sleep$group, labels=c("control","treatment"))

> summary(sleep)

extra group ID

Min. :-1.600 control :10 1 :2

1st Qu.:-0.025 treatment:10 2 :2

Median : 0.950 3 :2

Mean : 1.540 4 :2

3rd Qu.: 3.400 5 :2

Max. : 5.500 6 :2

(Other):8

> with(sleep, tapply(extra, group, mean)) # just a quick check

control treatment

0.75 2.33

> attach(sleep) # looks like I got it right, so reattach

Here is the t-test (treating the scores as if they were from independent

samples).

> t.test(extra ~ group, var.eq=T)

Two Sample t-test

data: extra by group

t = -1.8608, df = 18, p-value = 0.07919

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-3.363874 0.203874

sample estimates:

mean in group control mean in group treatment

0.75 2.33

We'll use these results as if they were from a pilot study. We now want to know

what we have to do to get a publishable result here (i.e., p < .05), assuming

our pilot data reasonably represent nature. We didn't quite reach statistical

significance with n = 10 per group. How many subjects/group should we use to

get a power of 80%?

The power.t.test() function gives us a way to

get some idea of the answer. The function wants to be fed several arguments:

n = the number of subjects/group, delta = the anticipated difference between

the means, sd = the anticipated pooled standard deviation of the two groups,

sig.level = the significance level we desire for the test, type = the type of

t-test we will use ("two.sample" is the default), and alternative = the nature

of the alternative hypothesis ("two.sided" is the default). Exactly one of those

arguments should be set to NULL, and the function will estimate it for us from

the other values.

> power.t.test(n=NULL, delta=1.58, sd=1.9, sig.level=.05, power=.8)

Two-sample t test power calculation

n = 23.70004

delta = 1.58

sd = 1.9

sig.level = 0.05

power = 0.8

alternative = two.sided

NOTE: n is number in *each* group

We are being told to use 24 subjects/group. We've made the usual t-test

assumptions of sampling from normal distributions and equal variances. But

the variances were not quite equal in our samples. The SDs were 1.8 and 2.0.

Let's use those values to get an estimate of power from a Monte Carlo

simulation. We will simulate drawing samples of 24 from normal distributions

with means and SDs equal to those we saw in our sample.

What we are about to do is, perhaps, best done with a script. That way, if

something goes wrong, we don't have to re-enter multiple lines into the R

Console. However, we will live on the edge for the sake of illustration. To

get this to work with minimal effort on our part--always a good thing--we will

need to get R to do the same set of calculations many times. This is done with

a loop, and in R, loops are most often done using

for(). The syntax is

"for (counter in 1 to number of simulations)". The statements to be looped

through repeatedly then follow enclosed in curly braces. I feel a bit like I'm

trying to describe an elephant to someone who's never seen one before. Perhaps

it would be best to just show you the elephant.

> R = 1000

> alpha = numeric(R)

> for (i in 1:R) {

+ group1 = rnorm(24, mean=.75, sd=1.8)

+ group2 = rnorm(24, mean=2.33, sd=2.0)

+ alpha[i] = t.test(group1, group2, var.eq=T)$p.value

+ }

The first line defines the number of random simulations we want and stores this

value in the semi-official data object that R typically uses for such things,

namely R. We've done 1000 sims, because that's the number that is normally done.

Some people use R=999, others use 10,000, just because they can. Computers are

pretty fast these days. 1000 usually gives a reasonably accurate result.

The second line creates a numeric vector with 1000 elements, which will hold the

result of each simulation. The third line begins our "for loop": "for i (the

counter) going from 1 to 1000", do the following stuff. I.e., do the following

stuff 1000 times, keeping track by incrementing the counter, i, at each

step. Group 1 is generated. Group 2 is generated. The t-test is done, and the

p-value is extracted and stored in "alpha", our designated storage place. In

each simulation, the storage occurs in the ith position of the alpha

vector. The loop was executed as soon as we typed the close curly brace. Now

all that remains is to determine how many of those values are less than .05.

> mean(alpha < .05)

[1] 0.787

To do this, we played a nice little trick. Remember, "alpha<.05" generates a

logical vector of TRUEs and FALSEs, in which TRUEs count as ones and FALSEs

count as zeros. We took the mean of that vector, which is to say, we calculated

by a bit of trickery the proportion of TRUEs. Our simulation tells us we have

a 78.7% chance of rejecting the null hypothesis under these conditions,

not quite the 80% that we desired. Your results will differ, of course,

because we are using a randomizing procedure after all.

Notice this made quite a mess of your workspace.

> ls()

[1] "alpha" "group1" "group2" "i" "R" "sleep"

> rm(alpha, group1, group2, i, R)

You might want to clean up a little bit.

Doing It With boot()

In the "boot" library there is a function,

boot(), which supposedly automates this process and makes it more

convenient. The library is not loaded at start-up, so first we have to load it.

> library("boot")

I should point out, at least for simple bootstraps,

I don't see how this method is in any

way "convenient." You still have to write your own functions, even when the

function you want is one that is predefined in R. Seems to me that doing it

this way can actually be MORE work than what we've just done.

Nevertheless, glutton for punishment that I am, I will see if I can get it

to work. Here is the syntax for boot, and

good luck to you if you have only the help page to guide you!

boot(data, statistic, R, sim = "ordinary", stype = c("i", "f", "w"),

strata = rep(1,n), L = NULL, m = 0, weights = NULL,

ran.gen = function(d, p) d, mle = NULL, simple = FALSE, ...,

parallel = c("no", "multicore", "snow"),

ncpus = getOption("boot.ncpus", 1L), cl = NULL)

Okay, got it?

Nope! I can't find any way to make

boot() actually do this. The help page

says the function generates bootstrap replicates, so let's see what that's

about.

Update

This might do it, but it took a lot of trickery, and I'm not sure it's

right. See the section below on parametric bootstrap for an explanation. (This

method seems quite obtuse compared to the method that was presented in the previous

section, so I'm not going to put a lot of effort into explaining it!)

> ran.gen = function(data, mle) {

+ c(rnorm(24, mean=.75, sd=1.789), rnorm(24, mean=2.33, sd=2.002))

+ }

> alpha = function(data, i) {

+ t.test(data[1:24], data[25:48], var.eq=T)$p.value

+ }

> fakevect = rnorm(48, mean=1.54, sd=1.9)

> b.out = boot(data=fakevect, statistic=alpha, R=1000, sim="parametric", ran.gen=ran.gen)

> mean(b.out$t < .05)

[1] 0.792

The estimated power for groups of 24 each is 79.2%.

The Bootstrap

Bootstrap resampling makes no assumptions about the populations other than

what we can know from the samples. Bootstrapping treats the samples as

mini-populations and resamples from them with replacement to get what are called

bootstrapped samples. These bootstrapped samples are then used to get p-values,

estimates of population parameters, confidence intervals, etc. Above, in the

"sleep" example, we acknowledged that the variances of the two samples were not

homogeneous, but we still assumed that we were sampling from normal

distributions. How did we know that? We didn't. (That's why it's called an

assumption!) Let's acknowledge that as well.

Here is a bootstrapped sample from sleep$extra, group 1. (I still have

"sleep" attached. If you don't, attach it. If you do, DON'T attach it again!)

> sample(extra[1:10], size=24, replace=T)

[1] 3.4 -0.1 3.7 -0.1 0.7 -0.2 0.0 0.7 3.4 0.7 3.4 0.8 3.7 3.4 2.0 0.7

[17] 0.0 -0.1 -0.2 -0.1 3.7 -1.2 -0.2 -1.2

Your result will be different because sample()

takes a random sample from the specified population (first argument). The

critical feature here is the sample is taken with replacement. Let's see how

many times we can get an alpha less than .05 if we do this from both groups

and calculate a t-test. Once again, use a script window if you're uncertain

that you can type this correctly on the first try.

> R = 1000

> alpha = numeric(R)

> for (i in 1:R) {

+ group1 = sample(extra[1:10], size=24, replace=T)

+ group2 = sample(extra[11:20], size=24, replace=T)

+ alpha[i] = t.test(group1, group2, var.eq=T)$p.value

+ }

> mean(alpha < .05)

[1] 0.844

The bootstrap is telling us we're okay here with samples of 24 each if we want

a power of at least 80%. This is not necessarily a "different" result than

the one we got above, because this is based on random (re)sampling, after all,

and we will get a different answer every time we do it. You got a different

answer than I did, right? I just ran it three more times, however, and my

answers are pretty consistently 83-86%, which I have to assume means we are

seeing a difference when we resample from the original data without making the

normality assumption. Since we didn't make any assumptions about the parent

population, this is called a nonparametric bootstrap.

> detach(sleep) # and clean up; keep sleep

"Automating" It With boot()

Here's one way you could do the same thing with the boot() function, and I'm going to show you this just

to illustrate how the function works, sort of. Bear with me if you know better.

The function will require three pieces of information

from you: the name of the data set (vector, matrix, or data frame), a function

that YOU have written that defines the statistic you want to have bootstrapped,

and R. I'll call my function "alpha", give it the "sleep" data frame, and I

also have to give it an i, which the function will use internally to

keep track of what iteration it's on. (Note: I detached sleep before I did this.)

> alpha = function(sleep, i) {

+ group1 = sample(sleep$extra[1:10], 24, replace=T)

+ group2 = sample(sleep$extra[11:20], 24, replace=T)

+ t.test(group1, group2, var.eq=T)$p.value

}

> boot.out = boot(data=sleep, statistic=alpha, R=1000)

> mean(boot.out$t < .05)

[1] 0.852

The model object, boot.out, contains a fair amount of information. Do

names(boot.out) to see it all and then don't worry

about most of it. The relevant

output, the p-values in this case, are in boot.out$t.

That's the equivalent of our alpha vector above.

You should be thinking, that was really a pointless exercise! Why wrap the

boot function around the same exact thing we did above without the boot function?

What's the point of that? I wanted to show you that you have to write your own

function to be used by boot, and that the output of that function, applied to

your data, is in t inside the

boot.out object. Other than that, you're right. It was quite pointless.

All we did was duplicate the action of the previous script, but we let boot

store the results for us. There's gotta be more to it than that, right?

The problem that boot() has with this example

is that we are trying to draw bootstrap samples that are larger than the

original data vector. I've seen a few sources where they get around this by

using a script similar to the one earlier in this section. Most sources

recommend the parametric bootstrap (i.e., Monte Carlo similulation) for

doing power problems.

I might point out, however, that with 24 subjects per group and a two-tailed

t-test at alpha of .05, you would need an effect size of about 0.42 (Cohen's d)

to find a significant difference between the means. How often could we count on

getting an effect size that large or larger from data like these?

> cohensd = function(data, i) {

+ d = data[i,]

+ abs(t.test(d$extra ~ d$group, var.eq=T)$statistic * sqrt(2/10))

+ }

> boot.out = boot(data=sleep, statistic=cohensd, R=1000)

> mean(boot.out$t >= .42)

[1] 0.841

Now we see the boot() function in its element.

First, we need to write a function to calculate Cohen's d, and this one is

based on the easily verifiable fact that d = t * sqrt(2/n) when there are n

subjects per group in a t-test. The function is given two arguments, "data"

(which will be fed to the boot() function when

that is executed) and "i", the indexing variable. We will tell boot that

data=sleep, a data frame. The boot() function will

take care of permuting that for us. So we hand over each permuted data frame

to a variable called d, and then we use that to calculate a t-test, extract

the t-value with $statistic, and then multiply by sqrt(2/10) to convert it to

Cohen's d, which is always positive, so the absolute value is taken as well.

Then we feed the boot() function our data, our

function, and R, and let it do it's thing. And it tells us we have about an

84% chance of getting an effect this large or larger from data like these,

which is consistent with the last result. (Phew! It took me a long time to

think of that!)

Bootstrapping The t-Test

The idea is to consider the pooled

sample to be a mini-population of scores. Presumably, we were sampling from a

larger parent distribution, but we know nothing about it for certain. The only

information we have about the parent distribution is the sample we've obtained

from it. Under the null hypothesis, the two groups, control and treatment, were

effectively sampled from the same population. Thus, we pool the two samples to

emulate that population as best we can.

Then we simply bootstrap two samples from that mini-population and see how

likely it is to get a result more extreme than the one we actually observed.

We'll need some sort of statistic to determine "extremeness." The difference

between means would be adequate. We'll do that below.

It would actually be a little easier to just let R calculate t-values from

our bootstrapped samples. That will require a little more internal effort from

our hardware, but since computing power is more than up to the task these days,

what do we care? There's also an educational lesson here (students!). The

problem with just calculating a t-test and looking up critical values in the

back of the book is that, if we haven't met the assumptions of the test, then

our calculated value of t will not be distributed theoretically as t, so

comparing our calculated t to the tables will be a bit off.

Therefore, we will calculate a new sampling distribution for the test

statistic by resampling from our mini-population WITH replacement, calculating

the desired statistic, and taking a look at what we get. (Notice that since we

pooled the samples, we are still sort of making a homogeneity of variance

assumption by doing this. We are also beginning with the assumption that the

null hypothesis is true.)

> with(sleep, t.test(extra ~ group, var.eq=T)$statistic) # for reference

t

-1.860813

> scores = sleep$extra # the data

> R = 1000 # the number of replicates

> t.star = numeric(R) # storage for the results

> for (i in 1:R) {

+ group1 = sample(scores, size=10, replace=T)

+ group2 = sample(scores, size=10, replace=T)

+ t.star[i] = t.test(group1, group2, var.eq=T)$statistic

+ }

The (estimated or approximated or simulated) sampling distribution

of the t-statistic can be visualized in a histogram, and I will plot the

obtained t-value as a point on the x-axis. Finally, I'll draw a line over it

showing the theoretical t-distribution for df=18.

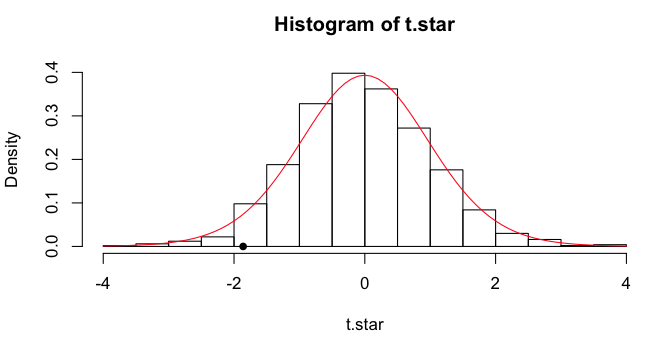

> hist(t.star, freq=F)

> points(x=-1.8608, y=0, pch=16)

> lines(x<-seq(from=-4, to=4, by=.1), y=dt(x, df=18), col="red")

We can get some quantiles.

We can get some quantiles.

> quantile(t.star, c(.025,.05,.5,.950,.975))

2.5% 5% 50% 95% 97.5%

-1.92422717 -1.65896181 -0.07050922 1.62722956 2.09215955

The simulation p-value is obtained as previously.

> mean(t.star <= -1.8608) # one-tailed

[1] 0.031

> mean(abs(t.star) >= 1.8608) # two-tailed

[1] 0.065

Our reference two-tailed p-value from the "actual" t-test is 0.079.

Automating It With boot()

Let's bootstrap the actual t-test. (Btw, you can bet I'm typing this into

a script window!)

> boot.tee = function(data, i) {

+ d = data[i,]

+ c(t.test(d$extra[1:10], d$extra[11:20], var.eq=T)$statistic,

+ t.test(d$extra[1:10], d$extra[11:20], var.eq=T)$p.value)

+ }

> boot.out = boot(data=sleep, statistic=boot.tee, R=1000)

Here's the explanation. First, I defined a function called boot.tee, which is

a function of the data and i. Our boot.tee function will find out what

the "data" are when we tell that to boot(). I

handed each permuted value of the

data to a variable called d. (I don't know if this is standard, but it's a

trick I learned in Zieffler, et al, and I thought it was very clever.)

Then I created a vector

containing two output values: the t-value from the t-test, and p-value from

that test. Notice when I did that, I did not use a formula interface, DV~IV.

I would do that if I was starting with the assumption that the alternative

hypothesis is true, as that would cause group 1 values to be bootstrapped

from group 1, and group 2 values to be bootstrapped from group 2 of the

original data. In other words, when the data frame is permuted, all columns of

it are permuted, so scores (extra) remain paired with the group from whence

they came in any given row of the permuted data. Instead, I was starting with

the assumption that the null

hypothesis is true. I let boot permute the data frame into a random order,

jumbling up the rows in the process,

and then I tested the first ten scores against the last ten.

If I want to check to see if this function is working properly, I can run

it on the original data frame and see if it gives me the right answers.

> boot.tee(sleep)

t

-1.86081347 0.07918671

Then I ran the boot() function (and immediately got an error because it's

a new day, and I forgot to load the "boot" library). Let's see what we got.

> boot.out

ORDINARY NONPARAMETRIC BOOTSTRAP

Call:

boot(data = sleep, statistic = boot.tee, R = 1000)

Bootstrap Statistics :

original bias std. error

t1* -1.86081347 1.8628096 1.0646010

t2* 0.07918671 0.4121642 0.2867875

I get output for both items I calculated as part of the statistic. First, t1*

is the t-value, and second, t2* is the p-value. The first thing I'm told is

what the values are when the function is run on the original data ("original").

Then I'm told how far off the bootstrapped values are from that ("bias"), on

the average. Finally, I'm given the standard deviation of the 1000 bootstrapped

value ("std. error").

> summary(boot.out$t) # boot.out$t is a matrix in this case

V1 V2

Min. :-4.029412 Min. :0.0007866

1st Qu.:-0.685015 1st Qu.:0.2468949

Median :-0.011462 Median :0.4913727

Mean : 0.001996 Mean :0.4913510

3rd Qu.: 0.722583 3rd Qu.:0.7358411

Max. : 3.242622 Max. :1.0000000

The actual bootstrapped values are inside boot.out in a variable called t, so

I asked for a summary of that. V1 is the first thing I calculated (t-value),

and V2 is the second thing I calculated (p-value). Notice that the means in both

cases are equal to original + bias from the first output. For finer grained info,

we'll run quantile(), and we MUST remember to ask

for a specific column of the t matrix. Otherwise, we'll be getting quantiles

from the t-values and p-values all mixed together. Not useful!

> quantile(boot.out$t[,1], c(.025,.05,.5,.95,.975))

2.5% 5% 50% 95% 97.5%

-2.02421421 -1.75560123 -0.01146238 1.77771580 2.10951478

The result is very similar to what we got in t.star, but not exactly the same

because this was a new set of permutations of the data. The p-values also

differ a bit.

> mean(boot.out$t[,1] < -1.8608) # one-tailed

[1] 0.038

> mean(abs(boot.out$t[,1]) >= 1.8608) # two-tailed

[1] 0.081

Note: There is a function in

the "boot" library called boot.ci(), but the

output doesn't agree with above, and I'm not sure why. As usual, the help

page wasn't much help. The explanation is NOT that the output object is a

matrix, because it doesn't work (for me) if only one stat is calculated. So

I don't use this function!

Here is an example of how to use it from stackoverflow.com.

> x <- rnorm(100, 1, .5)

> b <- boot(x, function(u,i) mean(u[i]), R = 999)

> boot.ci(b, type = c("norm", "basic", "perc"))

BOOTSTRAP CONFIDENCE INTERVAL CALCULATIONS

Based on 999 bootstrap replicates

CALL :

boot.ci(boot.out = b, type = c("norm", "basic", "perc"))

Intervals :

Level Normal Basic Percentile

95% ( 0.962, 1.206 ) ( 0.961, 1.205 ) ( 0.963, 1.206 )

Calculations and Intervals on Original Scale

> quantile(b$t,c(.025,.975)) # for comparison

2.5% 97.5%

0.9632601 1.2059236

Seems to work here. Didn't work above. Good luck!

Note: When a test statistic such as a Student's t is bootstrapped,

Zieffler, Harring, and Long (2011, see refs) call

this bootstrapping using a pivot statistic (p. 163). They imply that it's a

bit safer than the parametric bootstrap, which is outlined below, because

fewer population parameters must be "known."

Bootstrapping The Difference in Means

Assuming the Null Hypothesis is True

First, we'll combine all the DV values into one "population" and pull

both bootstrap samples from that. Our obtained value for the difference in

means is 1.58, for reference.

> mean.diff = function(data, i) {

+ d = data[i,]

+ mean(d$extra[11:20]) - mean(d$extra[1:10])

+ }

> mean.diff(sleep) # test function on original data

[1] 1.58

> boot.out = boot(data=sleep, statistic=mean.diff, R=1000)

> quantile(boot.out$t, c(.025,.05,.5,.95,.975))

2.5% 5% 50% 95% 97.5%

-1.72025 -1.44050 -0.04000 1.44050 1.67025

> mean(boot.out$t >= 1.58) # one-tailed p-value

[1] 0.035

> mean(abs(boot.out$t) >= 1.58) # two-tailed p-value

[1] 0.068

The bootstrapped 95% CI on the mean difference values consistent with the null

is -1.72 to 1.67. This interval includes the reference value.

In this case, we handed our function the data (to be specified in boot) and

an indexing variable i, we passed off the current (ith) bootstrap of the

data to d. The data is to be a data frame, so two indices are needed on data[i,].

The first index, i, contains a bootstrapped sample of the rows 1:20. The second

is blank, which means all columns. Since the rows of the data have now been

randomly permuted, or actually randomly bootstrap sampled, any arbitrary 10

values can be used to calculate the first mean, and the other 10 values the

second mean. The easiest way is 11:20 for the first mean and 1:10 for the

second mean, or vice versa. (Note: This method is illustrated by Zieffler

et al, p. 160.)

The same procedure without boot() would look

like this.

> data = sleep

> R = 1000

> results = numeric(R)

> for (i in 1:R) {

+ indices = sample(1:20, size=20, replace=T)

+ d = data[indices,]

+ results[i] = mean(d$extra[11:20]) - mean(d$extra[1:10])

+ }

> quantile(results, c(.025,.05,.5,.95,.975))

2.5% 5% 50% 95% 97.5%

-1.66000 -1.40150 -0.00500 1.41050 1.70025

> mean(abs(results) >= 1.58)

[1] 0.067

Not Assuming the Null Hypothesis is True

This time we will take bootstrap samples from the individual groups. For

reference, the obtained mean difference is 1.58, and the parametric 95%

confidence interval is -0.20 to +3.36.

> mean.diff = function(data, i) {

+ d = data[i,]

+ mean(d$extra[d$group==2]) - mean(d$extra[d$group==1])

+ }

> mean.diff(sleep) # test function on original data

[1] 1.58

> boot.out = boot(data=sleep, statistic=mean.diff, R=1000, strata=sleep$group)

> quantile(boot.out$t, c(.025,.05,.5,.95,.975))

2.5% 5% 50% 95% 97.5%

-0.03000 0.23950 1.61000 2.87000 3.09075

> mean(boot.out$t <= 0) # one-tailed p-value

[1] 0.028

The bootstrapped 95% CI on the mean difference is -0.03 to 3.09, a little

narrower than the parametric value. I've run this many times, and the lower

bound of the CI jumps back and forth across 0. Even at R=10000, the lower

bound can't quite decide which side of 0 it wants to be on. So this is a

close one.

When the order of rows in the data frame is permuted (bootstrapped), the

group information remains with the data values. So this time the mean.diff

function calculates the difference between a mean of values that came from

group 2 and a mean of values that came from group 1. The strata= option is

not actually necessary to make the procedure run and give an answer, but it

seems to make a slight difference in the width of the CI, so I'm not

sure how it's used, but it should be included to tell the procedure that the

two groups are being sampled separately. (Note: This method is illustrated by

Zieffler et al, p. 190.)

The same procedure without boot() would look

like this.

> data = sleep

> R = 1000

> results = numeric(R)

> for (i in 1:R) {

+ indices = sample(1:20, size=20, replace=T)

+ d = data[indices,]

+ results[i] = mean(d$extra[d$group==2]) - mean(d$extra[d$group==1])

+ }

> quantile(results, c(.025,.05,.5,.95,.975))

2.5% 5% 50% 95% 97.5%

0.0248750 0.1899048 1.5415862 2.9043119 3.1559799

> mean(results <= 0)

[1] 0.024

Important note: How do you get a poor result from a bootstrap? Use small

samples. While I've used a small sample case above to illustrate the methods,

you should probably be wary of using bootstrap in such cases.

Permutation and Randomization Tests: The Jackknife

I will use the sleep data to illustrate our

next topic as well, which is permutation tests.

The logic behind a permutation test is straightforward. It says, "Okay, these

are the twenty (in this example) scores we got, and the way they are divided up

between the two groups is one possible permutation of them. There are, in

fact...

> choose(20,10)

[1] 184756

...possible permutations (technically combinations--but same idea) of these

data into two groups of ten, and each is equally likely to occur if we were to

pick one at random out of a hat. Most of these permutations would give no or

little difference between the group means, but a few of them would give large

differences. How extreme is the obtained case?" In other words, the logic of

the permutation test is quite similar to the logic of the t-test. If the

obtained case is in the most extreme 5% of possible results, then we reject the

null hypothesis of no difference between the means (assuming we were looking at

differences between means). The advantage of the permutation test is, it does

not make any assumption about normality, and in fact, doesn't make any

assumption at all about parent distributions. Furthermore, a permutation test

is generally more powerful than a "traditional" nonparametric test.

The disadvantage of a permutation test is the number of permutations that

must be generated. Even small samples, as we have here, will choke a typical

desktop computer with repetitive calculations. Therefore, instead of generating

all possible permutations, we generate only a random sample of them. This

procedure is often called a "randomization test" instead of a permutation test.

Let's see the elephant, and then I'll explain.

> ### Begin by cleaning up your workspace, if you haven't already.

> R = 1000

> scores = sleep$extra

> t.star = numeric(R)

> for (i in 1:R) {

+ index = sample(1:20, size=10, replace=F)

+ group1 = scores[index]

+ group2 = scores[-index]

+ t.star[i] = t.test(group1, group2, var.eq=T)$statistic

+ }

First, we set the number of

sims (replications, resamplings) to 1000. Then we made a copy of the data, which

was really unnecessary. Then we established a storage vector for the results of

the sims. Then we began looping. Inside the loop, we took a random sample of the

vector 1 to 20, without replacement, and stored that in an object called

"index". These index values were then used to extract the first resampled group

of scores. The second group of scores was extracted using a trick, which in

words goes, "for group two take all the scores that are not indexed by the

values in index." In other words, put the remaining scores in group two. Then we

did the t-test and stored the test statistic (t-value). It now remains to

compare those simulated t-values to the one we obtained above when we did the

actual t-test.

> mean(abs(t.star) >= 1.8608) # two-tailed test

[1] 0.072

The resampling scheme tells us that a little more than 7% of the sims gave us a

result as extreme or more extreme than the obtained case. This is the p-value

resulting from the randomization test. We can see that it is pretty close to the

p-value obtained in the actual t-test above (.0794). The difference may be

nothing more than random noise. (Note: Once again, your result will be

different due to the randomization done by sample().)

The bootstrap method simulates random sampling from a population. The

randomization method, sometimes called jackknife resampling, simulates random

assignment to groups. It's usually considered the preferred method if your

subjects are volunteers or you snatched them out of the hallway during

change of classes.

Another Way

There are as many ways to do randomization tests as there are statistics

you can think up to assess the difference between the groups. Here is another

way. Notice in this case I've use a different, but equally effective, method

of resampling as well. I merely rearrange (permute) the scores and use the

original grouping variable to index them.

> R = 1000

> scores = sleep$extra

> groups = sleep$group

> mean.diff = numeric(1000)

> for (i in 1:R) {

+ perm.scores = sample(scores, size=20)

+ mean.diff[i] = diff(tapply(perm.scores, groups, mean))

+ }

> tapply(scores, groups, mean)

1 2

0.75 2.33

> 2.33 - .75 # the obtained difference

[1] 1.58

> mean(abs(mean.diff) >= 1.58)

[1] 0.086

The result is similar. We'd get a narrower range of results if the

samples were larger.

Paired Scores

"Hey! These are paired scores. Deal with that!" First, let's get some

reference info from the standard t-test for paired scores.

> t.test(extra ~ group, data=sleep, paired=T)

Paired t-test

data: extra by group

t = -4.0621, df = 9, p-value = 0.002833

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-2.4598858 -0.7001142

sample estimates:

mean of the differences

-1.58

The logic behind randomization in this case is that it is a matter of chance

which of the paired scores occurred in the control group and which occurred in

the treatment group. In other words, when we look at the sign on the difference

scores, it's a coin flip as to whether than sign will be positive or negative.

The difference scores are...

> diffs = sleep$extra[1:10] - sleep$extra[11:20]

> diffs

[1] -1.2 -2.4 -1.3 -1.3 0.0 -1.0 -1.8 -0.8 -4.6 -1.4

...and a lot of them are negative, but the null hypothesis says that's just

dumb luck. Given that those are the difference scores, it's a matter of pure

chance what sign they have. And there is the randomization we need to justify

a randomization test.

> R = 1000 # we'll do 1000 sims

> absdiffs = abs(diffs) # strip the signs

> results = numeric(R) # create a storage vector

> for (i in 1:R) { # begin looping

+ sign = sample(c(1,-1), 10, replace=T) # get 10 random signs

+ results[i] = mean(absdiffs * sign) # get mean of diffs with new signs

+ }

> quantile(results, c(.025,.975)) # 95% of them fall in what interval?

2.5% 97.5%

-1.16 1.14

> mean(abs(results) >= 1.58) # two-tailed p-value

[1] 0.006

The result is not too different from what the t-test revealed. You can

completely clear your workspace now. We are done with "sleep".

About Those p-Values

Some sources propose that the p-values derived as above are ever so slightly

too small and that a correction should be applied that can be calculated like

this.

p.corrected = (pR + 1) / (R + 1)

Where p is the probability as calculated above and R is the number of

replications. With R = 1000, the largest correction this will ever result in

is less than .001, which is undoubtedly well within the boundaries of

uncertainty on the p-value anyway. To apply a correction to the third or

fourth decimal place of a value that's probably not entirely accurate in the

second decimal place strikes me as being a little fussy. But there you have it.

Use it as you see fit. With a smaller number of reps, it could be important.

Note on terminology: As we are taking a random sample of possible

permutations of the data in the jackknife, jackknife resampling can reasonably

be referred to as Monto Carlo resampling, and often is.

Bootstrapped Confidence Intervals

Bootstrap resampling is useful for estimating confidence intervals from

samples when the sample is from an unknown (and clearly nonnormal) distribution.

The data set "crabs" in the MASS package supplies an example. We will look at

the carapace length of blue crabs.

> data(crabs, package="MASS")

> cara = crabs$CL[crabs$sp=="B"]

> summary(cara)

Min. 1st Qu. Median Mean 3rd Qu. Max.

14.70 24.85 30.10 30.06 34.60 47.10

> length(cara)

[1] 100

> qqnorm(cara) # not shown

Hmmmm, that looks reasonably normal to me, but who can say for sure? So to get

a 95% CI for the mean, we will use a bootstrap scheme rather than methods based

on a normal distribution. But just for reference purposes, the normal

distribution method would give the following result.

> t.test(cara)$conf.int

[1] 28.68835 31.42765

attr(,"conf.level")

[1] 0.95

The procedure is to take a large number of bootstrap samples and

to examine the desired statistic.

> R = 1000

> boot.means = numeric(R)

> for (i in 1:R) {

+ boot.sample = sample(cara, 100, replace=T)

+ boot.means[i] = mean(boot.sample)

+ }

> quantile(boot.means, c(.025,.975))

2.5% 97.5%

28.71027 31.37937

The bootstrapped CI is reasonably close to the one obtained by traditional

methods, so the normal approximation seems to be reasonable for these data.

Extension to more complex problems is straightforward.

Doing It With boot()

I have to admit that using boot() may be just

a smidge easier in this case.

> boot.means = function(cara, i) {mean(cara[i])}

> boot.out = boot(data=cara, statistic=boot.means, R=1000)

> quantile(boot.out$t, c(.025,.975))

2.5% 97.5%

28.75858 31.39305

But certainly no less cryptic! It may also be useful just too look at the

output of boot() directly.

> boot.out

ORDINARY NONPARAMETRIC BOOTSTRAP

Call:

boot(data = cara, statistic = boot.means, R = 1000)

Bootstrap Statistics :

original bias std. error

t1* 30.058 0.015603 0.6902185

The value "original" is the mean of the original data

vector "cara". The value "bias" gives the difference between "original" and the

mean of the bootstrapped values for this statistic. Clearly, "bias" ought to be

close to zero. The value "std. error" is the standard deviation of the

bootstrapped means.

Bootstrapping is more usefully applied to statistics like the median, for

which there is no formula for CIs when the distribution is not normal.

> boot.medians = function(cara, i) {median(cara[i])}

> boot.out = boot(data=cara, statistic=boot.medians, R=1000)

> quantile(boot.out$t, c(.025,.975))

2.5% 97.5%

27.85 32.40

> boot.out

ORDINARY NONPARAMETRIC BOOTSTRAP

Call:

boot(data = cara, statistic = boot.medians, R = 1000)

Bootstrap Statistics :

original bias std. error

t1* 30.1 0.08145 1.461501

Clean up your workspace. It's a mess!

The Parametric Bootstrap

So far, and in future sections as well, what we've been doing is called the

nonparametric bootstrap, because no assumptions are being made about population

parameters. We will use some data from the MASS package to illustrate an

alternative method called the parametric bootstrap.

> data(birthwt, package="MASS")

> head(birthwt)

low age lwt race smoke ptl ht ui ftv bwt

85 0 19 182 2 0 0 0 1 0 2523

86 0 33 155 3 0 0 0 0 3 2551

87 0 20 105 1 1 0 0 0 1 2557

88 0 21 108 1 1 0 0 1 2 2594

89 0 18 107 1 1 0 0 1 0 2600

91 0 21 124 3 0 0 0 0 0 2622

> bw = birthwt[,c("smoke","bwt")] # we need only these two columns

> bw$smoke = factor(bw$smoke, labels=c("no","yes"))

> summary(bw)

smoke bwt

no :115 Min. : 709

yes: 74 1st Qu.:2414

Median :2977

Mean :2945

3rd Qu.:3487

Max. :4990

>rm(birthwt)

The data show birthweights (bwt) in grams of babies born to mothers who

smoked and mothers who did not smoke. The obvious point of interest is,

what's the difference, if any, in the mean birthweights for the two groups?

Let's look at the data.

> with(bw, tapply(bwt, smoke, mean))

no yes

3055.696 2771.919

> with(bw, tapply(bwt, smoke, var))

no yes

566492.0 435118.2

> plot(density(bw$bwt[bw$smoke=="yes"])) # not shown

> lines(density(bw$bwt[bw$smoke=="no"]),col="red")

The means are different by a bit more than 280 grams. The variances are also

different, but not too much. The last two lines of code plot overlapping

kernel density

estimates of the distributions, which show that both of them are mound shaped

and not too terribly different from normal. Thus, we will assume that both

groups were sampled from the same normal distribution that has parameters

equal to the sample mean and variance. (We are assuming the null hypothesis

is true, and that our "bwt" variable is sampled from a single normal

distribution.)

The first step is to create a DV that consists of standardized values as if

they were drawn from a single population with a mean of 0 and a standard

deviation of 1. This can be done with the scale()

function.

> bw$z.bwt = scale(bw$bwt)

Now we'll investigate the difference between the two groups on this variable.

> with(bw, tapply(z.bwt, smoke, mean))

no yes

0.1523672 -0.2367869

> with(bw, diff(tapply(z.bwt, smoke, mean)))

yes

-0.3891541

The difference is almost four tenths of a standard deviation. The syntax for

the parametric bootstrap is:

boot(data, statistic, R, sim="parametric", ran.gen)

The last two options are new. One of them obviously tells R that we want a

parametric bootstrap. The other one is another function that we have to write

to generate Monte Carlo samples from the standard normal distribution

(assuming it is the normal distribution that we have decided fits our data).

bwt.gen = function(data, mle) {

rnorm(n=length(data))

}

I have no idea why the mle is necessary, but it is. As usual, we also need the

function that calculates our test statistic.

mean.diff = function(data, i) {

mean(data[1:115]) - mean(data[116:189])

}

Since we've generated a random vector of standard scores in bwt.gen, I just

took the difference in means between the first 115 of them (representing

nonsmokers) and the last 74 of them (representing smokers). Once those

functions are executed and in the workspace, we can run boot().

> boot.out = boot(data=bw$z.bwt, statistic=mean.diff, R=1000, sim="parametric", ran.gen=bwt.gen)

The results are in the usual place.

> boot.out

PARAMETRIC BOOTSTRAP

Call:

boot(data = bw$z.bwt, statistic = mean.diff, R = 1000, sim = "parametric",

ran.gen = bwt.gen)

Bootstrap Statistics :

original bias std. error

t1* 0.9683415 -0.965374 0.1527679

> summary(boot.out$t)

V1

Min. :-0.553122

1st Qu.:-0.099277

Median : 0.006685

Mean : 0.002968

3rd Qu.: 0.104059

Max. : 0.504965

> quantile(boot.out$t, c(.025,.975)) # does not contain 0.3891541, so yay!

2.5% 97.5%

-0.3040931 0.3042744

> mean(abs(boot.out$t) >= 0.3891541) # two-tailed p-value

[1] 0.011

For the record, the parametric p-value from the t-test is .0087.

It seems to me that "parametric bootstrap" is just a new name for

Monte Carlo simulation. How are they different?

Bootstrapping a Regression Analysis

First, thanks to John Fox for a very clear example of how to use boot() here, which I found in a document posted

here. Here is where the boot()

function is going to shine, I have to admit. We will look at a problem that we

also examine in the Multiple Regression tutorial,

in which we attempt to predict life expectancy by U.S. state using various

predictors (1977 data).

> states = state.x77

> states = as.data.frame(states) # must be a data frame

> colnames(states)[c(4,6)] = c("Life.Exp","HS.Grad") # fix some variable names

> lm(Life.Exp ~ Murder + HS.Grad + Frost, data=states) # for reference

Call:

lm(formula = Life.Exp ~ Murder + HS.Grad + Frost, data = states)

Coefficients:

(Intercept) Murder HS.Grad Frost

71.036379 -0.283065 0.049949 -0.006912

First, we define a function to get the statistic(s) we want, which are the

regression coefficients.

> boot.states = function(states, i) {

+ mod = lm(Life.Exp ~ Murder + HS.Grad + Frost, data=states[i,])

+ coefficients(mod)

+ }

Once again, the data are not just "states" but states[i,] from the ith

iteration of the bootstrap. Now it remains to run

boot() and examine the output.

> boot.out = boot(data=states, statistic=boot.states, R=1000)

> boot.out

ORDINARY NONPARAMETRIC BOOTSTRAP

Call:

boot(data = states, statistic = boot.states, R = 1000)

Bootstrap Statistics :

original bias std. error

t1* 71.036378813 -0.1117470290 1.111679000 # intercept

t2* -0.283065168 0.0050440366 0.040044342 # Murder slope

t3* 0.049948704 0.0009847503 0.017462937 # HS.Grad slope

t4* -0.006911735 0.0002284539 0.003021178 # Frost slope

> summary(boot.out$t)

V1 V2 V3 V4

Min. :66.42 Min. :-0.3927 Min. :0.002082 Min. :-0.016386

1st Qu.:70.29 1st Qu.:-0.3056 1st Qu.:0.039119 1st Qu.:-0.008695

Median :71.03 Median :-0.2824 Median :0.050579 Median :-0.006672

Mean :70.92 Mean :-0.2780 Mean :0.050933 Mean :-0.006683

3rd Qu.:71.69 3rd Qu.:-0.2548 3rd Qu.:0.061776 3rd Qu.:-0.004735

Max. :73.49 Max. :-0.1007 Max. :0.122853 Max. : 0.003244

> quantile(boot.out$t[,2], c(.025,.975)) # 95% CI for Murder slope

2.5% 97.5%

-0.3452561 -0.1883249

> quantile(boot.out$t[,3], c(.025,.975)) # compare this to boot.ci() answer below

2.5% 97.5%

0.01702089 0.08657885

> confint(lm(Life.Exp ~ Murder + HS.Grad + Frost, data=states)) # parametric CIs for comparison

2.5 % 97.5 %

(Intercept) 69.05717472 73.015582905

Murder -0.35700149 -0.209128849

HS.Grad 0.01935043 0.080546980

Frost -0.01183825 -0.001985219

> boot.ci(boot.out, type="perc", index=3) # still doesn't give quite the right answer

BOOTSTRAP CONFIDENCE INTERVAL CALCULATIONS

Based on 1000 bootstrap replicates

CALL :

boot.ci(boot.out = boot.out, type = "perc", index = 3)

Intervals :

Level Percentile

95% ( 0.0169, 0.0867 )

Calculations and Intervals on Original Scale

Now, clean up your workspace in preparation for the next and final section,

but KEEP the states data frame. We're going to use it again.

Resampling a Oneway ANOVA

We will begin by adding a factor, census region, to the "states" data frame,

which hopefully you still have left over from the last section. We're going to

change the value labels on the fly because, once again, spaces in the variable

names! Whose idea was that? (Note: state.region is a built-in data object.)

> states$Region = factor(state.region, labels=c("Northeast","South","Midwest","West"))

> summary(states)

Population Income Illiteracy Life.Exp Murder

Min. : 365 Min. :3098 Min. :0.500 Min. :67.96 Min. : 1.400

1st Qu.: 1080 1st Qu.:3993 1st Qu.:0.625 1st Qu.:70.12 1st Qu.: 4.350

Median : 2838 Median :4519 Median :0.950 Median :70.67 Median : 6.850

Mean : 4246 Mean :4436 Mean :1.170 Mean :70.88 Mean : 7.378

3rd Qu.: 4968 3rd Qu.:4814 3rd Qu.:1.575 3rd Qu.:71.89 3rd Qu.:10.675

Max. :21198 Max. :6315 Max. :2.800 Max. :73.60 Max. :15.100

HS.Grad Frost Area Region

Min. :37.80 Min. : 0.00 Min. : 1049 Northeast: 9

1st Qu.:48.05 1st Qu.: 66.25 1st Qu.: 36985 South :16

Median :53.25 Median :114.50 Median : 54277 Midwest :12

Mean :53.11 Mean :104.46 Mean : 70736 West :13

3rd Qu.:59.15 3rd Qu.:139.75 3rd Qu.: 81162

Max. :67.30 Max. :188.00 Max. :566432

> boxplot(Income ~ Region,states) # not shown

> with(states, tapply(Income, Region, mean))

Northeast South Midwest West

4570.222 4011.938 4611.083 4702.615

> with(states, tapply(Income, Region, sd))

Northeast South Midwest West

559.0771 605.4505 283.0825 663.9004

The relationship we are interested in is Income by Region (in case you didn't

guess). It looks like we have some pretty substantial differences here,

particularly between the South and the other regions. It also looks like we

have heterogeneous variances.

Monte Carlo Simulation

Let's use a Monte Carlo simulation to get an F.star distribution assuming the

null hypothesis is correct, and the four regions are actually samples from one

and the same population, and assuming normality and homogeneity as well.

> data.star = states$Income

> mean.star = mean(data.star)

> sd.star = 555.0118 # the pooled standard deviation obtained from aov()

> IV.star = factor(rep(c("NE","S","MW","W"), times=c(9,16,12,13)))

> R = 1000

> F.star = numeric(R)

> for (i in 1:R) {

+ DV.star = c(rnorm(9, mean=mean.star, sd=sd.star),

+ rnorm(16, mean=mean.star, sd=sd.star),

+ rnorm(12, mean=mean.star, sd=sd.star),

+ rnorm(13, mean=mean.star, sd=sd.star)) # a little silly, but...

+ F.star[i] = oneway.test(DV.star ~ IV.star, var.eq=T)$statistic

+ }

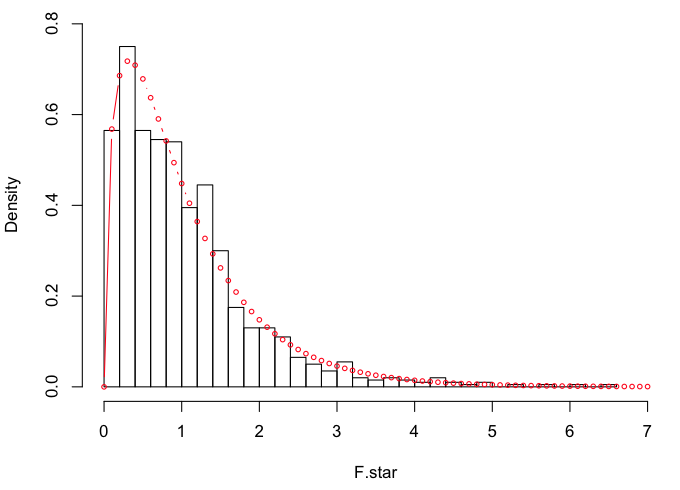

We should now have our simulated F-distribution (F.star) for df=3,46. I'll plot

it and then draw the theoretical F(3,46)-distribution over top of it.

> hist(F.star, breaks=30, prob=T, xlim=c(0,7), ylim=c(0,.8))

> points(x<-seq(0,7,.1), y=df(x,3,46), type="b", cex=.6, col="red")

They are very similar, which is not surprising given the way F.star was

created. For reference:

They are very similar, which is not surprising given the way F.star was

created. For reference:

> oneway.test(Income~Region, data=states, var.eq=T)

One-way analysis of means

data: Income and Region

F = 4.687, num df = 3, denom df = 46, p-value = 0.006136

> mean(F.star >= 4.687) # p-value

[1] 0.006

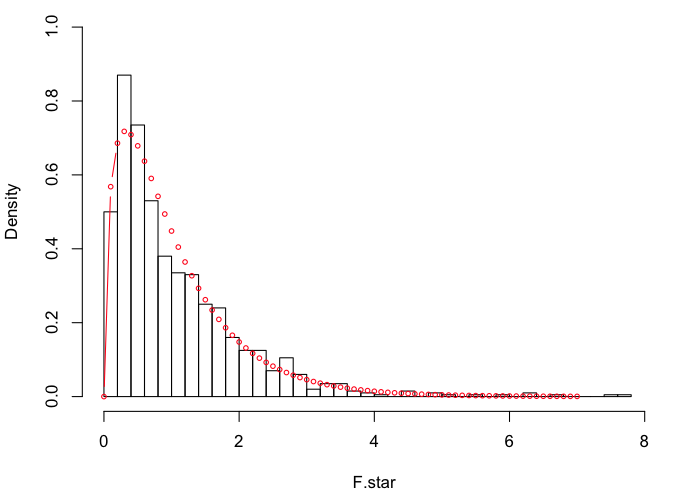

That's as close as we could come given 1000 sims. Let's do it again assuming

equal means but not assuming equal variances. For reference:

> oneway.test(Income ~ Region, data=states)

One-way analysis of means (not assuming equal variances)

data: Income and Region

F = 4.2638, num df = 3.000, denom df = 22.377, p-value = 0.01596

> R = 1000

> F.star = numeric(R)

> for (i in 1:R) {

+ DV.star = c(rnorm(9, mean=mean.star, sd=559.08),

+ rnorm(16, mean=mean.star, sd=605.45),

+ rnorm(12, mean=mean.star, sd=283.08),

+ rnorm(13, mean=mean.star, sd=663.90))

+ F.star[i] = oneway.test(DV.star ~ IV.star, var.eq=T)$statistic

+ }

> hist(F.star, breaks=30, prob=T, xlim=c(0,8), ylim=c(0,1))

> points(x<-seq(0,7,.1), y=df(x,3,46), type="b", cex=.6, col="red")

Looks like we might be a little heavier in the tails this time.

Looks like we might be a little heavier in the tails this time.

> qf(.95, 3, 46)

[1] 2.806845

> quantile(F.star, .95) # okay, maybe not

95%

2.78404

> mean(F.star >= 4.2638) # p-value

[1] 0.013

Randomization Test

One key assumption of the randomization test, not previously mentioned, is

exchangeability. Basically, this means that a subject who ended up in one group

could just have easily have ended up in some other group. The only way to

guarantee exchangeability is to do random assignment to groups. Thus, the

randomization test is often reserved for true, randomized experiments. With

intact groups, it's hard to say that a Missourian could just have easily been

a Californian, or that California could just as easily have ended up in the

Midwest. (They do have some rather "interesting" earthquakes out there. Just

saying, speaking as a person who used to live there!) Nevertheless, just to

illustrate the method, we're going to assume exchangeability.

> income = states$Income # just making the data a little more accessible

> region = states$Region

> R = 1000 # 1000 reps (good thing we're not doing pushups!)

> results = numeric(R) # a place to store the results

> for (i in 1:R) {

+ permuted.income = sample(income, size=50, replace=F)

+ results[i] = oneway.test(permuted.income ~ region)$statistic

+ }

> mean(results >= 4.2638) # F = 4.2638 is the result from the real data

[1] 0.022

Assuming the null hypothesis is true, and permuting (resampling without

replacement) the income values 1000 times, we find the probability of getting a

result greater than or equal to the observed one is 0.022. The test was done

without assuming homogeneity of variance.

Let's Try boot()ing It

Zieffler et al suggest that a good statistic to bootstrap for an ANOVA is

the effect size, eta-squared. Others have suggested the treatment sum of squares,

the treatment mean square, and the variance of the treatment means. As these are

all functions of F and the degrees of freedom, it seems to me that they should

give the same result as bootstrapping F (degrees of freedom being constants for

any given problem). Let's find out.

> aov(income ~ region)

Call:

aov(formula = income ~ region)

Terms:

region Residuals

Sum of Squares 4331342 14169750

Deg. of Freedom 3 46

Residual standard error: 555.0118

Estimated effects may be unbalanced

> 4331342/3

[1] 1443781

> var(tapply(income, region, mean))

[1] 97939.1

First we get some reference values. SST = 4331342. MST = 1443781. VarT =

97939.1. I'm going to store these, because I don't want to have to remember

them.

> SST = 4331342

> MST = 1443781

> VarT = 97939.1

> Eta2 = 4331342 / (4331342 + 14169750) # eta-sq = 0.2341128

> Fobs = (4331342/3) / (14169750/46) # assuming homogeneity, F = 4.687021

I'm having second thoughts about the variance of the treatment means, given

that this is an unbalanced design. I think it would work if the design were

balanced. Now we have to write a function, to be used by the bootstrap, that

calculates all these things. To make life easier, I'm going to get rid of the

original data frame, make a new one from just the variables we're using, and

then erase those from the workspace.

> rm(states)

> states = data.frame(income, region)

> rm(income, region)

Okay, here we go!

> SS = function(x) sum(x^2) - sum(x)^2/length(x) # a function for sum of squares

> boot.states = function(data,i) {

+ d = data[i,]

+ aov.out = aov(d$income ~ states$region)

+ SST.star = SS(d$income) - SS(aov.out$residuals)

+ MST.star = SST.star / 3

+ VarT.star = var(tapply(d$income, states$region, mean))

+ Eta2.star = SST.star / SS(d$income)

+ F.star = MST.star / (SS(aov.out$residuals)/46)

+ c(SST.star, MST.star, VarT.star, Eta2.star, F.star)

+ }

> boot.states(states) # looks like our function passes the test

[1] 4.331342e+06 1.443781e+06 9.793910e+04 2.341127e-01 4.687020e+00

> bout = boot(data=states, statistic=boot.states, R=1000)

> summary(bout$t)

V1 V2 V3 V4 V5

Min. : 4453 Min. : 1484 Min. : 3649 Min. :0.0002858 Min. :0.004383

1st Qu.: 460119 1st Qu.: 153373 1st Qu.: 75190 1st Qu.:0.0260488 1st Qu.:0.410097

Median : 881114 Median : 293705 Median :112246 Median :0.0495693 Median :0.799704

Mean :1145724 Mean : 381908 Mean :120906 Mean :0.0632042 Mean :1.088080

3rd Qu.:1533472 3rd Qu.: 511157 3rd Qu.:156216 3rd Qu.:0.0879430 3rd Qu.:1.478482

Max. :9006160 Max. :3002053 Max. :390738 Max. :0.3856425 Max. :9.624990

Alright! Drove myself a little crazy with that one for awhile! Until I discovered

that the proper ANOVA was not aov.out = aov(d$income ~ d$region). That would be

assuming the null hypothesis is false. We are assuming the null hypothesis is

true, so we have to do the ANOVA against the original (unbootstrapped)

arrangement of region. Same thing for the variances of the treatment means (of

course). Zieffler also calculated eta-squared from the original

SS Total rather than the bootstrapped one, as I have above. I'm not sure what

the justification is for that. Now for the moment of truth.

> mean(bout$t[,1] >= SST)

[1] 0.019

> mean(bout$t[,2] >= MST)

[1] 0.019

> mean(bout$t[,3] >= VarT)

[1] 0.031

> mean(bout$t[,4] >= Eta2)

[1] 0.009

> mean(bout$t[,5] >= Fobs)

[1] 0.009

Here's what we've learned. Bootstrapping SST and MST give the same result.

That's not surprising since one is a linear transform of the other. The

variance of the group means would also give the same result if the design

were balanced, because it is MST/n per group in those cases. In the many runs

of this I did, the bootstrap of the treatment variances consistently resulted

in the highest p-value, in this unbalanced case. The unbalanced

design has, appropriately, cost us a little power. Bootstrapping

eta-squared gives the same result as SST and MST if the original SS

Total is used to calculate it (as per Zieffler et al). If not, it gives the same

result as bootstrapping

the F statistic (as here and as expected, as it is a linear transform of F).

Bootstrapping the F statistic consistently gives a

slightly smaller p-value than bootstrapping SST and MST (and Eta2 if the original

SS Total is used to calculate it).

revised 2016 March 6; updated March 8

| Table of Contents

| Function Reference

| Function Finder

| R Project |

|